QUOTE(Alison @ Thu 9th December 2010, 7:17pm)

QUOTE(TungstenCarbide @ Thu 9th December 2010, 6:10pm)

QUOTE(Alison @ Fri 10th December 2010, 1:44am)

This guy knows the truth.

grumpy old guy is right but missing part of the story. Much of economics is driven by psychology. After the great depression people thought credit was evil. You wanted a car ... save your money and pay cash. Nowadays most people choose to live their whole lives with large credit loads.

Easy credit is like a drug, some people can't get enough of it and end up bleeding themselves dry. Governments have been making credit easier and easier for decades.

That's also true. Interesting article

here which shows the situation in 2004. Back then, they were stating that nearly 43% of American families spend more than they earn each year. So yeah - not good, but where does the blame lie; government or wide-eyed, gullible people?

"Call 1-800-YOU-FAIL begin_of_the_skype_highlighting              1-800-YOU-FAIL      end_of_the_skype_highlighting to get the credit you deserve!"

Deserve?? How many times have they played those adverts on TV? And they're always aimed at people with already bad credit ratings

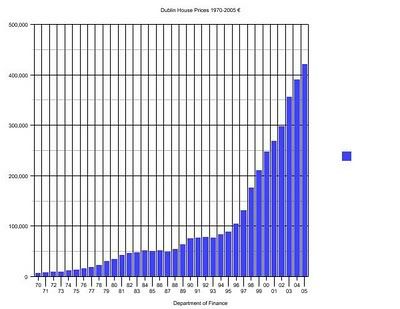

Sigh. The Irish situation is a duplicate of the US one, already much-discussed here. During the 2000-2007 housing bubble, both the US and Ireland (I mean the good people of both countries) borrowed a lot of money against their inflating housing prices. The new financial instruments (which HK calls generic "derivatives") made it easier than ever to convert real estate "paper-equity" into cash. One of those derivatives was insurance on securitized mortgage backed loans. You could even buy

stock in companies

that sold insurance on securitized mortgage backed loans.

Like AIG. Level piled upon level of speculation there, and it all collapsed in 2008 when the markets simply could not take any more, and all the loaned out money on housing that wasn't worth it, came due to be repaid. In both the US and Ireland, since the capital markets around the world are all connected too well now for any to be isolated.

2004 was right in the middle of this. How could 43% of American families (or Irish families if you like, because it was all the same there) spend more than they earned each year? No problem in 2004 at the height of this rising housing bubble. It wasn't going all on credit cards, but coming out of houses being used like ATM machines, as second and third mortgages became available. There even existed plastic cards that gave you money from a loan against your house (a home equity line of credit-- try to get one of THOSE now). Nobody cared about this, before the housing equity values (on paper) were going up faster than the home loan borrowers were spending the money; it was sort of like spending money you were making on your stock account in your portfolio.

Except that everyody knows such rises in stock value are imaginary numbers until you lock in the earnings by actually

selling the stock. In housing speculation people weren't actually

selling their houses even though they were speculating with them in just the same way as with stock-- they were just watching their

paper value rise, and borrowing against THAT, and spending it.

When it all came crashing down in 2008, people owed more on their houses than they were worth. In Ireland, too. HK thinks the banks got all that money, but he's wrong. The people who borrowed against the housing market, which means the home-owners, got most of that money. Letting banking systems collapse now that they own the titles to all the real estate left behind (the "ash" of this bubble), is not going to fix this problem. The blame for all this is everywhere. A lot of it is with homeowners who had a great time with the money they "made" speculating against their own home prices as they rocketted up.

If you can let your banking system collapse, which means that your industry is not far behind, then your economy goes down and everybody is out of work. Not just 10% but 25% or more. They tried that 1929-1932 in the U.S., and it didn't work so well. Tight-money made the depression worse. Bernanke, a student of the depression, is therefore now trying the opposite, which is to put all the housing credit default on the government credit card. So far it has kept the US economy from imploding.

Now it's Ireland's turn. They (like the U.S.) have a total government debt of about 100% of their yearly GDP. But this next year, if they bail out all the housing market lenders (and yes, most of them are banks, who will foreclose on the houses) that will go up to 133% of GDP. They will have spent 33% of a year's GDP in a SINGLE YEAR, bailing themselves out. The US did almost that last year, but it put them only up to 94% GDP. Ireland's debt position is worse.

But they don't really have any choice. If they allow the housing sector, mortgage lenders and banks to take the default on all that credit, there won't be any more banking in Ireland. Which means no more Irish economy, no more Irish industry, and no more Irish miracle. So they're going to have to do what the U.S. did, or else have a Great Depression of 1929. Were it not for the suffering that would cause, I'd wish that they actually would do that, just to teach HK and LaRouche a lession that they seem to have failed to learn from 1929-32.

I doubt that's the half of it.

Looking from a different angle, if you were a group of powerful bankers who had enormous political power at your fingertips, what kind of laws would you get your lackeys to pass to enrich yourself? Those laws would have to be based on human psychology.

You'd want to make it possible for people to load themselves up on credit, to the hilt. Then you'd want their home to hang in the balance - keeping one's home is a big motivator (these lines of credit weren't legal when I was a kid.) Then you'd want them to shoulder the maximum amount of credit for as long as possible to bleed them over a lifetime.

How much of the US GDP went into soybeans? Did our investment increase that much in any other sector you can think of, from 1998 to 2006? I'll give you the answer: no. So single thing sapped as much investment money, by turning it into capital and then cash, as the housing market. Nothing else was that big.

How much of the US GDP went into soybeans? Did our investment increase that much in any other sector you can think of, from 1998 to 2006? I'll give you the answer: no. So single thing sapped as much investment money, by turning it into capital and then cash, as the housing market. Nothing else was that big.

. We don't know how much of that went on. We do know that Citigroup, Merrlll Lynch, and Morgan Stanley got $6 trillion in quicky-loans between just the three of them (what-- you think they KEPT it??), whereas your average mainstreet business got nothing, and (if you weren't a Fannie or Freddie mortgage), your mortgage didn't get affected either.

. We don't know how much of that went on. We do know that Citigroup, Merrlll Lynch, and Morgan Stanley got $6 trillion in quicky-loans between just the three of them (what-- you think they KEPT it??), whereas your average mainstreet business got nothing, and (if you weren't a Fannie or Freddie mortgage), your mortgage didn't get affected either.